We all know it can be difficult to save money. There are

many bills to pay, and immediate needs make saving money a challenge not only

for you but for everyone. However, many people do not realize the benefit of

compounding interest, and when you do not save regularly you are missing out on

a great opportunity.

The two most important pieces to financial success are time

and regular savings. The news media spends a lot of time discussing investments

and unique ways to be financially prepared for life, all of which are important

for an individual to have a truly healthy financial future. However, nothing is

more important than starting early and benefiting from the power of compound

interest.

A simple definition of interest is a payment received for

the use of one’s money. Often this is a bank paying you interest on the money

you have deposited in your savings or checking account. This can also be

interest earned from an investment in a stock or mutual fund.

By definition, compound interest is: interest paid on both

the principal and on previously earned interest, which doesn’t sound very

impressive or impactful until you look at the numbers.

Let’s look at a simple example:

Many people have a savings account that might be earning a

small amount of interest. Below is how compound interest can affect the value

of a savings account:

- For this example, Mary puts $1,000 into a savings account

that earns 3% interest each year. After the first year Mary would have earned

$30 in interest, so her account balance would be $1,030 (3% multiplied by

$1,000).

- In the second year, Mary would earn $30.90 in interest,

$30 in interest on the $1,000 deposited and $0.90 on the $30 in interest she

earned last year. If Mary would have taken out the interest she received in

year one, then she would have missed out on the $0.90 in interest in year two.

- In year three, not only does she get to earn interest on

the original $1,000, but she also earns interest on the $30 earned in year one

and now Mary earns interest on the $30.90 she earned in year two.

After 10 years, Mary’s balance would be $1,343.92, if all of

the interest were allowed to compound. If Mary had withdrawn the $30 interest

each year, she would have $1,000 in the account and only $300 in withdrawn cash;

that’s $43.92 extra from compound interest she would not have. After 30 years,

the difference would be $527.26.

Regular Savings

Now, let’s add in the second most important feature for

financial success, regular savings. If Mary adds just $5 per month to her

savings account, after 10 years her balance earning 3% interest would be

$2,031.75. After 30 years her balance would be $5,281.79.

One of the places you can see significant savings and

compounding is in your employer’s retirement plan. Taking advantage of your

employer’s plan is one of the best places to save.

If you do not have access to a retirement program, you can

take advantage of compounding interest and a regular savings program at your

local bank or investment services provider.

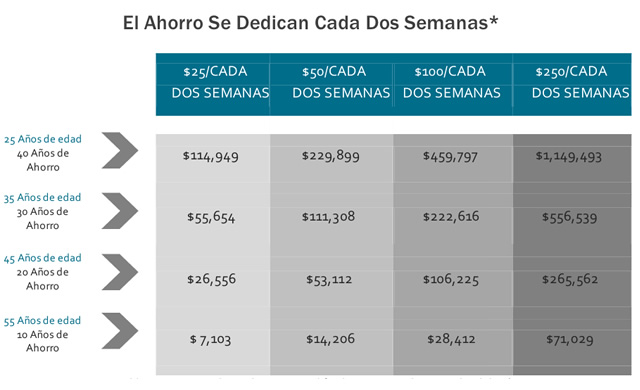

Below is a chart showing how quickly your savings can grow

when you set aside money on a regular basis.

*Note this chart represents tax-deferred savings in a

retirement type account, and does not account for taxes which will apply upon

distribution of accumulated savings. Assumptions: initial investment – zero

($0), 26 pay periods, and 6.5% annual return.

Allow compound interest to work for you by starting to save

as early and as often as you can!

Article sourced through SageView Advisory Group www.sageviewadvisory.com

Todos sabemos que puede ser difícil para ahorrar dinero. Hay muchas cuentas que pagar, y las necesidades inmediatas hacen ahorrar dinero un desafío no sólo para usted, sino para todo el mundo. Sin embargo, muchas personas no se dan cuenta del beneficio del interés compuesto, y cuando no los guardas regularmente se están perdiendo una gran oportunidad.

Las dos piezas más importantes para el éxito financiero son el ahorro de tiempo y regular. Los medios de comunicación pasa mucho tiempo hablando de las inversiones, y las formas únicas para estar preparado financieramente para la vida, todo es importante para una persona para tener un futuro financiero saludable. Sin embargo, nada es más importante que a partir de principios y beneficiarse del poder del interés compuesto.

Una definición simple de interés es un pago recibido por el uso de dinero de uno. Muchas veces se trata de un banco te paga intereses sobre el dinero que han depositado en sus ahorros o cuenta corriente. Esto también puede ser intereses ganados por la inversión en una acción o fondo mutuo.

Por definición, el interés compuesto es: los intereses pagados por tanto el principal como el interés ganado con anterioridad, que no suena muy impresionante o impactante hasta que nos fijamos en los números.

Veamos un ejemplo sencillo:

- Para este ejemplo, Mary pone $1,000 en una cuenta de ahorros que gana intereses 3% cada año. Después del primer año María habría ganado $30 en interés, la cuenta sería $1,030. (3% multiplicado por $ 1,000)

- En el segundo año, Mary ganaría $30.90 en intereses, $30 en intereses sobre los $1,000 depositado y $0.90 en los $30 en intereses que ganó el año pasado. Si Mary hubiera retirado el interés que recibió en el primer año, se habría perdido en los $0.90 en intereses en el segundo año.

- En el tercer año, no sólo se llega a ganar interés sobre el original de $1,000, pero también gana interés sobre los $30 obtenido en el primer año y ahora Mary gana intereses sobre el $30.90 obtuvo en el segundo año.

Después de 10 años, el balance de Mary sería de $1,343.92, si todo el interés que se les permitió compuesto. Si Mary había retirado el interés $30 por año, tendría $1,000 en la cuenta y sólo $300 en efectivo retirado, eso es $43.92 extra del interés compuesto. Después de 30 años, la diferencia sería $527.26.

Ahorro Periódico

Ahora, vamos a añadir en la segunda característica más importante para el éxito financiero, ahorro regular. Si Mary ahorra sólo $5 por mes a su cuenta de ahorros, después de 10 años el balance ganando interés del 3%, sería de $2,031.75. Después de 30 años el balance sería de $5,281.79.

Uno de los lugares que se pueden ver ahorros y de composición significativos es en el plan de jubilación de su empleador. Aprovechando el plan de su empleador es uno de los mejores lugares para ahorrar.

Si usted no tiene acceso a un programa de jubilación, usted puede tomar ventaja de la composición y un programa de ahorros en su banco local o el proveedor de servicios de inversión.

Abajo se muestra una tabla que muestra la rapidez con sus ahorros pueden crecer cuando se ahorra sobre una base regular.

Permita que el interés compuesto a trabajar para usted por comenzar a ahorrar tan pronto y con frecuencia como puedas!

Articulo de origen por medio de SageView Advisory Group www.sageviewadvisory.com

*Tenga en cuenta esta tabla representa un ahorro de impuestos diferidos en un tipo de cuenta de jubilación, y no tiene en cuenta los impuestos que se aplicaran sobre la distribución de los ahorros acumulados. Asunción: la inversión inicial – cero($0), 26 periodos de pago y retorno anual de 6.5%.

Post your Comment

Please login or sign up to comment

Comments